Karl T. Ulrich | Original Version June 15, 2018 | This Version February 26, 2024

This is a concise note describing the alpha asset framework, and intended for students and busy professionals. It may be reproduced and used for non-commercial purposes with citation. I am writing a book Alpha Assets: Building and Sustaining Competitive Advantage, but it’s not yet finished. Here also is a PDF version.

Here is a set of restaurant companies that are publicly traded in the United States. You’ll recognize many of these names, and in case you don’t know, Yum is the parent company of KFC and TacoBell among others.

As a group, they earned an average cash flow return on investment over the ten year period of 2006-2015 of about 6 percent per year. This measure of financial performance is the return on invested capital above and beyond each company’s weighted average cost of capital. This measure is sometimes called economic value added, or EVA.

But, why did those at the top earn so much more than those on the bottom? To some extent this is the most important question in business. For a given job to be done, how and why can an organization sustain competitive advantage and therefore earn an exceptional return on invested capital?

Of course something idiosyncratic can destroy a company or propel its fortunes. For instance, Yum brands made a huge bet on Asian markets and that bet paid off, and the great recession in the United States hurt some sit-down restaurants over the first five years of this period.

But fundamentally the only way one company can earn more than another over the long term is to experience some combination of greater demand, which is reflected in higher revenue, OR greater efficiency, which shows up as lower cost. Higher demand or lower cost. That’s it. But, how can one company enjoy greater demand than another, or lower costs? To do so, it must possess some resource or asset that enhances performance but that can not easily be acquired by its competitors. Yum has to have something special that PotBelly can not easily get.

Two such assets, fairly self-evident from the list of companies are: strong brands – say Starbucks – and huge scale – say McDonalds. I call these special types of resources a company’s alpha assets, a concept that is based on a key idea from the academic field of competitive strategy called the resource-based view of the firm.

I define alpha assets as resources owned or controlled by an organization that (a) enhance performance and that (b) are hard for others to acquire. Let’s take those two conditions in turn.

The presence of a performance-enhancing asset can uniquely cause significant improvements in profits relative to not having the asset, for most competitors. For example, electricity is a performance-enhancing asset for a restaurant company. Without electricity, your restaurant would likely be nothing more than a food cart on a street corner.

But can access to electricity be a source of competitive advantage? Probably not for a restaurant. Performance enhancement is a necessary condition for an asset to confer advantage, but it is not sufficient.

For restaurants, access to electricity can not be an alpha asset because that asset is not hard to acquire. All competitors can acquire electricity and so there will not be meaningful differences in its possession. (Although in some industries, say for computing infrastructure, perfect reliability of power is actually not that easy to acquire.)

An asset is hard to acquire when doing so requires a large amount of time, effort, or money, or is not possible at all.

For example, McDonald’s scale is essentially impossible for In-and-Out Burger to acquire in any reasonable amount of time or with any reasonable investment. And because scale is also performance enhancing, it is definitely an alpha asset.

Some assets can be hard to acquire, but not be performance enhancing. For instance, Starbucks is headquartered in Seattle. It would be expensive and take a long time for Luckin Coffee, a Chinese competitor to Starbucks, to move to Seattle. But, doing so would not significantly enhance performance, so the Seattle location is not an alpha asset for Starbucks.

I don’t have a precise technical definition for how much time and money comprises “hard to acquire” but you can think about required investments of say greater than 10 percent of revenue and/or time periods of five years or longer.

Let’s look at another example from another industry. Consider Amazon.

We’ve already discussed electricity and a Seattle headquarters – neither of these can be alpha assets for a restaurant or for Amazon. However, the Amazon brand confers advantage and can not be acquired by others. It’s an alpha asset. Amazon’s huge assortment of retailers on its platform confers advantage and is not easily acquired. It’s an alpha asset. Amazon’s vast trove of customer data is an alpha asset. Amazon’s massive scale is an alpha asset. And, although Amazon has embarked on a leadership transition, the founder, Jeff Bezos, has unambiguously been an alpha asset.

Some of you may criticize this framework for being unreasonably static. You are right. Almost no asset can remain alpha forever. That Chinese company, Luckin Coffee, pioneered the use of a mobile-first, all digital transaction system. In fact, I remember once trying to buy coffee in a shop in Shanghai and not having the app. The barista eventually abandoned the effort to set me up with the app and just gave me the coffee for free. Despite the barriers it imposed for foreign visitors, Luckin’s mobile-first strategy and implementation was an alpha asset for years. But, today, most coffee shops are fully app-enabled.

Where do alpha assets come from? In some cases, they come from an inventive spark or the conditions of the founding of the company. In other cases they are the result of good fortune. For example, if I can invoke an analogy, one of the alpha assets of Michael Phelps, the world champion swimmer, is his body dimensions, including his feet, which are US size 14 (or European size 48). Phelps didn’t do anything to acquire that alpha asset – it was endowed on him at birth. Similarly some alpha assets for companies are essentially random endowments, like when DuPont accidentally discovered the molecule polytetrafluoroethylene, which became its proprietary product Teflon.

But, more interesting are alpha assets that can be developed over time and as a result of deliberate action and managerial attention, such as cost efficiency or product performance. Fortunately these are the most important alpha assets in most organizational settings. These alpha assets are often the result of accumulation of strength via five mechanisms that I (and others) call flywheels. They represent tremendous sources of strength and resilience for organizations that can create them.

The Five Flywheels

In 2015, taking inspiration from Warren Buffet, I bought stock in Wells Fargo, one of the “big four” US banks. Oops. I’m now strictly an index investor, having learned my lesson watching the company’s stock decline over the next five years. Scandal after scandal plagued the bank. It seemed that every quarter some new crisis would arise. Yet, Wells Fargo has operated continuously since 1852. It seems pretty nearly impossible to kill this organization. In fact, it’s recovered again from its recent setbacks and its stock price is back up. (This of course after I sold my position. Go figure.) While few companies last as long as Wells Fargo, incumbent companies are remarkably resilient. If a company survives infancy, its prospects for living a few decades are very high, either as an independent company or as an operating unit within an acquiring company.

Why are incumbents so powerful, and how can a start-up chart a path to such strength?

I call the sources of incumbent power flywheels. In a physical system, a flywheel receives power and stores it as kinetic energy, which can then be tapped when and if necessary to overcome episodic demands.

An organization can also be thought of as a system, a machine for doing a job. It also has ways of accumulating energy.

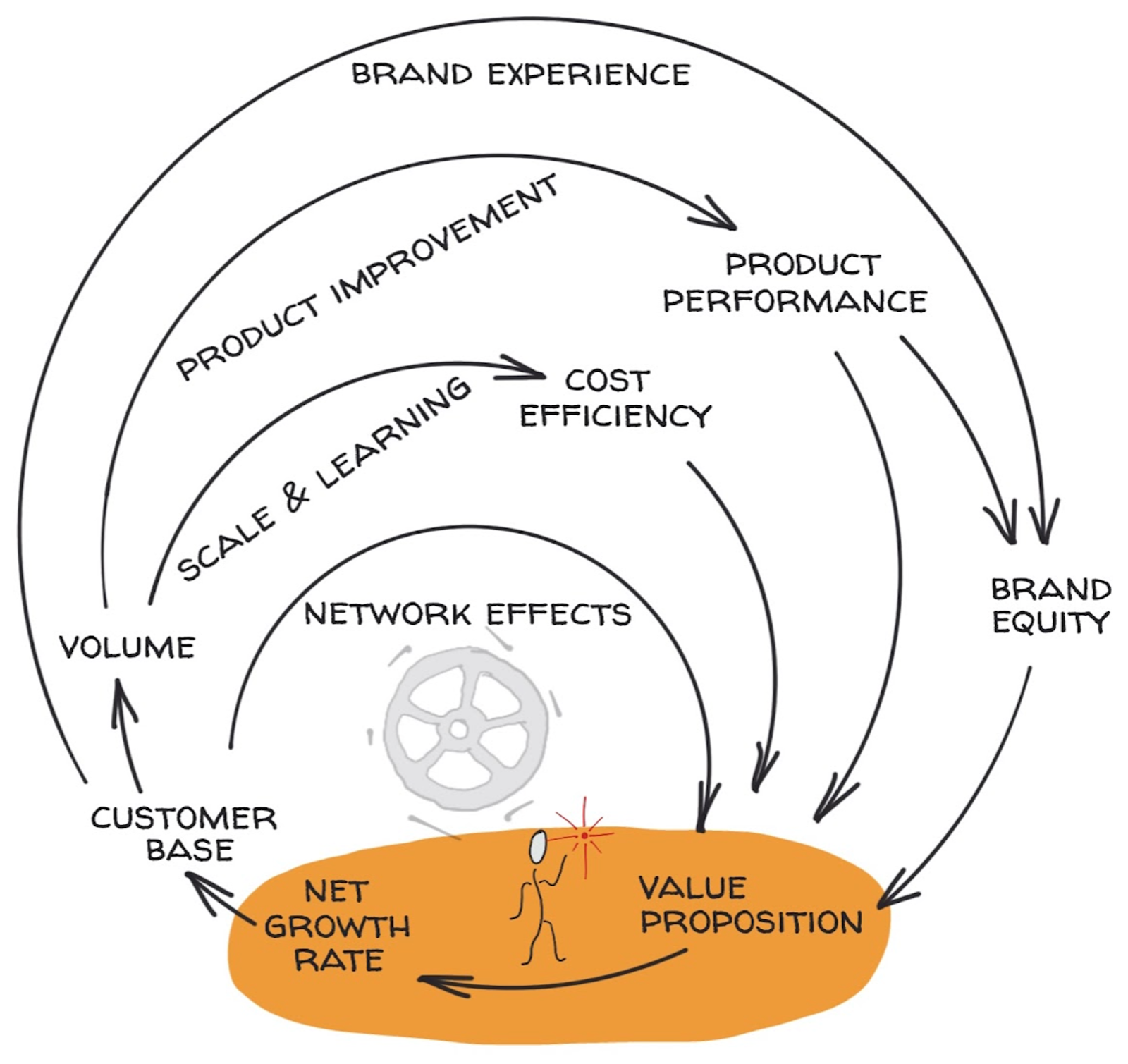

There are four flywheels that are almost always present to a greater or lesser extent in every company.

- Customer Network

- Cost Efficiency

- Product Performance

- Brand Equity

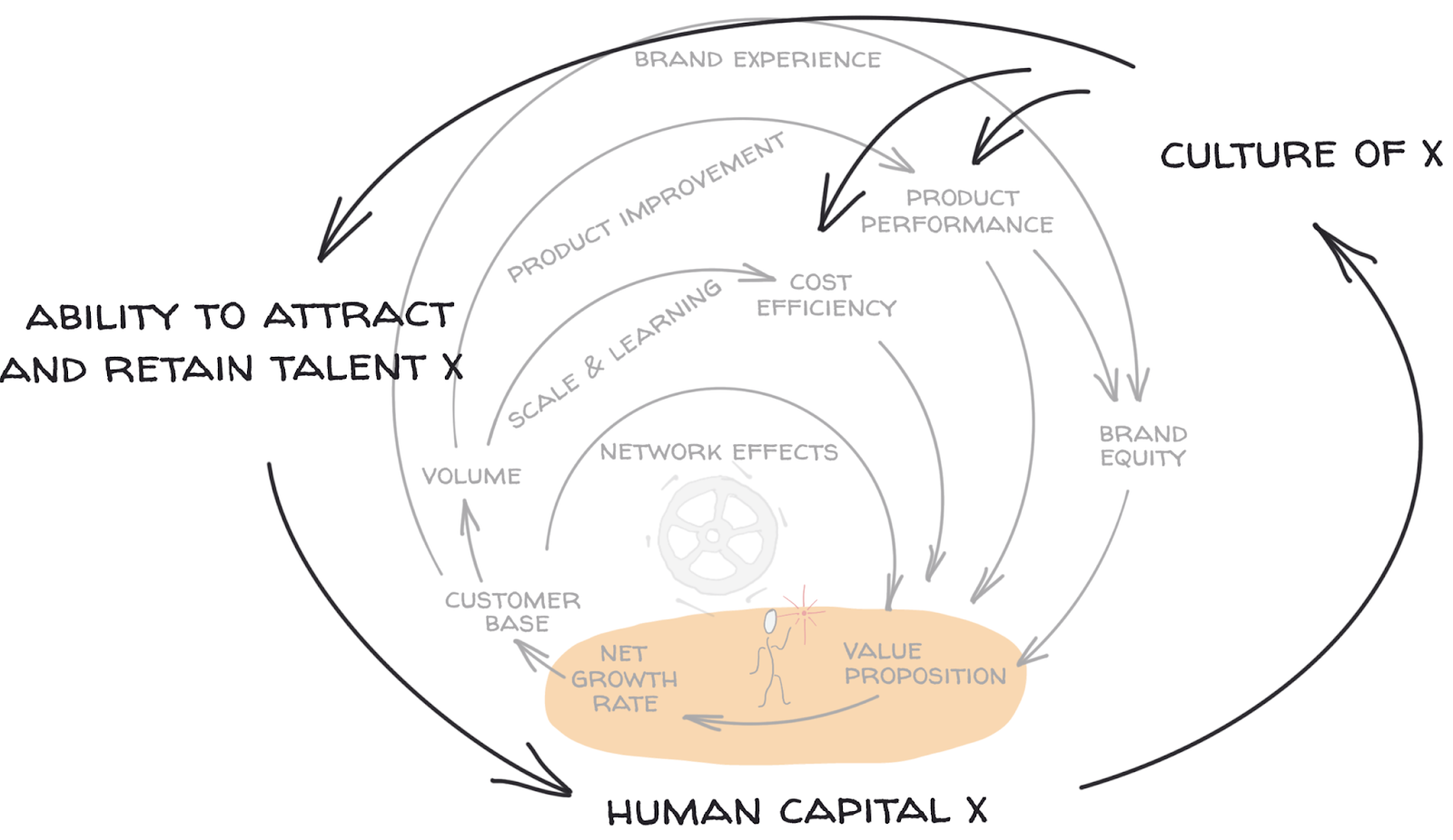

I’m going to add a fifth flywheel I call Organizational Capability and Culture. This fifth flywheel will reflect a focus of an organization on doing a few things well or on a distinctive culture.

Let me illustrate the first four flywheels with a graphic.

All businesses deliver a solution to a customer, and this essence of a business is what powers the flywheels. In order for the company to acquire customers it must offer a compelling value proposition and deliver on that value proposition through its customer experience. When and if the value proposition increases, the company’s rate of customer growth will also increase, and of course if the value proposition decreases, so will the rate of customer growth. Implicit is the reality that the net rate of customer growth depends both on acquiring new customers and on retaining existing customers, or minimizing so-called churn.

Delivering solutions with value is the engine powering the flywheels. Now, the flywheels themselves.

1 – Customer Network

The first flywheel is the customer network. This flywheel is important for products that enjoy network effects. Growth in new customers increases the number of customers in the customer base. For products with network effects, as the customer base increases, the value proposition of the product increases. This further increases the rate of customer growth. Not all products exhibit network effects. I enjoy drinking Peet’s coffee. The value proposition of Peet’s Coffee to me does not depend at all on how many other customers enjoy the same coffee. However, I also like the mobile payment app Venmo. It was useful to me when just my college-age children were users. But, Venmo became even more valuable when the guy who removes snow from my driveway became a user. Venmo is a product with huge network effects and really benefits from the first flywheel. (See James Currier’s article for a very thorough taxonomy of types of network effects.)

2 – Cost Efficiency

The second flywheel is cost efficiency. Cost efficiency improves with deliberate effort and the application of good process, but the biggest explanatory factors in lowering costs are cumulative units delivered and the current rate of production. Any organization that does something repeatedly can enjoy lowered costs because of the learning that occurs over time. This is called the learning curve. For example, just consider what happens as you take on any new task, say making a cup of coffee. The first time, it takes you 10 minutes as you figure out how to measure out the beans, heat the water, filter the brew, and clean up the mess. Now imagine you make 100 cups every morning working at a coffee bar. I’m pretty sure by the time you’ve made 1000 cups, you’ve figured out how to make each cup in less than a minute. That same kind of learning occurs in all organizations as the cumulative number of units produced increases. A second type of cost efficiency comes from scale economies. This is not the result so much of the cumulative number of units produced, but rather from the rate at which you produce them. If you are making 100 cups of coffee each hour you will adopt very different methods than if you are making 1 cup each hour. For example, you’ll invest in a big coffee grinder and massive drip brewing system. Those investments reap huge productivity improvements, but are only possible as the rate of production increases. Put this all together and you see the second flywheel at work – the unrelenting improvement in efficiency that comes both from accumulating experience and from investing in better processes enabled by increased scale.

3 – Product Performance

The third flywheel is product performance. Only the most tone deaf organization fails to improve its products with experience. A company observes where the customer complaints are and seeks ways to enhance its performance relative to rival products. These opportunities become a queue of product improvement projects and over time the product just keeps getting better.

In some settings, that product improvement flywheel leads to nearly insurmountable product performance advantages. For instance, the product of semiconductor company TSMC is a fabrication service it offers to chip designers like NVIDIA and Apple. Its primary alpha asset is the accumulated know-how and trade secrets embedded within its semiconductor fabrication process. For TSMC, product improvement is a flywheel propelled by powerful positive feedback – as its processes become more capable, its value proposition increases, and it wins the most demanding production challenges, further increasing its scale and learning, and making it even more likely to garner future orders. Some people believe that what TSMC does is the hardest single task in the world. No one else comes close to being able to do it. That product performance advantage is likely to persist for decades.

A proprietary product can in relatively rare settings be an alpha asset because of a legal monopoly obtained through patent protection or trade secrets. Patents as alpha assets exist primarily in the pharmaceutical industry in which a patented product is identical with a specific molecule for which regulatory agencies have granted approval for use. In such cases, the product performance advantage arises not from a flywheel of continual product improvement, but from a regulatory barrier. In most other settings, patents serve more as a deterrent to blatant copying, or as a tool for intimidating much smaller competitors with the threat of expensive legal action.

4 – Brand Equity

The fourth flywheel is brand equity. Especially for engineers, the notion of brand is pretty strange. Why is it that a label on a product can enhance the value proposition of a product? The short answer is that brand serves as a proxy for attributes of product quality that the consumer can not directly observe, brand reduces the time and effort required for a consumer to find and select products, and brand directly confers desirable brand associations to the consumer as a kind of badge. While these benefits are all intangible, brand is a shockingly powerful and therefore valuable alpha asset. Brand is a flywheel because the value of a brand, its brand equity, accumulates over time, and typically increases with market share, time in the market, and with improved product performance.

5 – Organizational Capability and Culture

Remember I said the fifth flywheel was the focus on a few organizational capabilities or elements of culture. Let me give you an example. When I was the Vice Dean of Entrepreneurship at Wharton, I led an organization of about 30 people. Early on, I placed a heavy emphasis on building an organization with a highly diverse workforce. I felt this was important in order to foster creativity and innovation and to best serve our student and alumni stakeholders, who were themselves a highly diverse population. A group of 30 middle-aged men who grew up in rural America like me was not my goal. As we worked to attract and retain staff who did not look or think like me, the diversity of our team increased. This diversity in turn made it much easier to attract and retain additional team members who didn’t fit the mold. After three or four years, the composition of our workforce became a source of high performance for us, and we became one of the most sought after places to work within the university, further enhancing our ability to attract and retain a talented and diverse team.

The fifth flywheel might comprise a culture of innovation, a culture of customer service, a passion for environmental sustainability, a focus on reliability, or almost any other distinctive element of organizational capability or culture. Such elements are very hard to acquire or build, and to the extent that they enhance performance, they can be alpha assets.

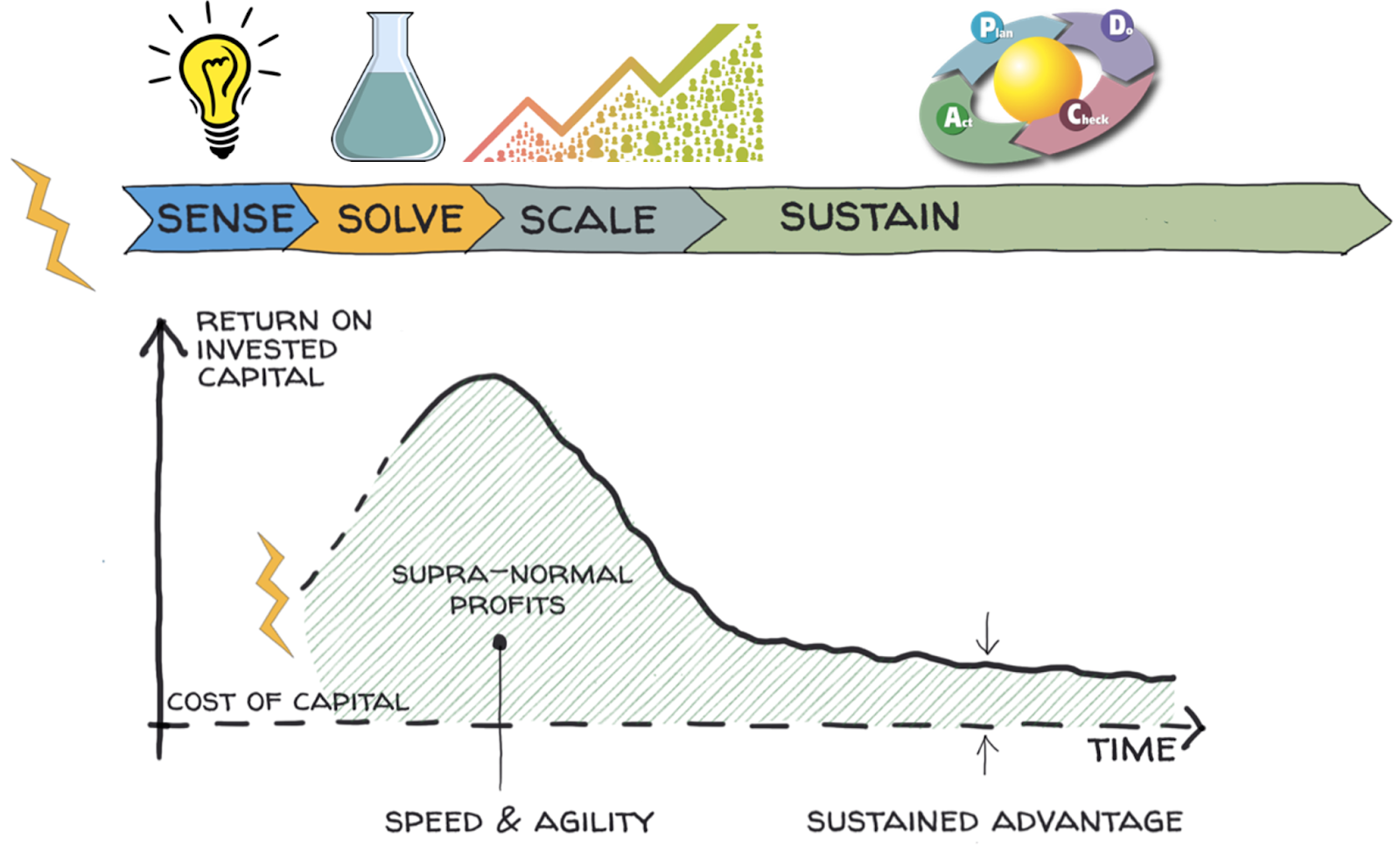

The Role of New Products in Kick Starting the Flywheels

Even Wells Fargo was once a start-up with flywheels at a standstill. How does a new enterprise get the flywheels going in the first place, and when does that company stand a chance against incumbents?

An idiosyncratic endowment of any single resource could in theory kickstart a flywheel, and therefore a company with advantage. For instance, when the musician John Legend co-founded LVE Collection Wines, he himself was the alpha asset for the company and immediately spun up a brand flywheel. However, this strategy is not available to the rest of us. More typically, a better mousetrap – a new product resulting from the invention of a new technology or the recognition of an emergent market need – is the alpha asset for a new company.

Peter Thiel famously wrote in his book Zero to One “as a good rule of thumb, proprietary technology must be at least 10 times better than its closest substitute in some important dimension to lead to a real monopolistic advantage.” The 10x rule is mostly rhetorical, but I do agree that when there is some disequilibrium in technology or in the market, then an organization has an opportunity to move with speed and agility to take advantage of that disequilibrium and to create a product that is dramatically better than the pre-existing alternatives. At the dawn of the covid pandemic of 2020, the videoconferencing company Zoom offered a product that just worked. It didn’t require registration. It didn’t require a download. It didn’t require any special gear. It just worked. Despite the fact that there were dozens of other solutions in the market at the time, including BlueJeans, Skype for Business, Google Hangouts, and WebEx, Zoom was able to seize the market and gain significant share. This was almost entirely because Zoom had a better product, at least on the important dimension of ease of use and reliability.

Better product is often an alpha asset for a relatively brief period following some type of disequilibrium. But, the organization must use this precious window of product superiority wisely in order to oversee the acceleration of the other flywheels for sustained advantage. Indeed, Zoom took advantage of its initial product performance and prospered. But, predictably Microsoft eventually followed with an improved enterprise product, Teams, that was at parity on many features and superior in others. Google was jolted awake and improved its product Meet as well. Zoom remains a key player, but its brand and customer network, perhaps even more than its product per se, have become its alpha assets.

In very dynamic markets – those for which some combination of enabling technologies, competitive actions, or customer behavior are changing very quickly – the organizational capability of product management can itself be an alpha asset. For example, consider the fitness app Strava. Strava does weekly product releases, which include incremental improvements and, less frequently, substantial product changes. Any particular version of the Strava app could likely be easily replicated by a team of developers and so the product per se is not much of an alpha asset. However, the system that Strava employs to engage its users, understand opportunities for improvement, and prioritize the changes in its product roadmap, benefits from experience with millions of users and a refined organizational process of product management. This organizational capability is an example of a fifth flywheel and a compelling alpha asset.

I need to be clear that not all things that are important are alpha assets. For example, an excellent sales process is very important for enterprise software companies. That doesn’t imply that a sales process could necessarily be a significant source of sustained competitive advantage. It’s more that if you fail to do sales well, you are unlikely to be successful in enterprise software. We could say the same thing about operational competence for a restaurant, or accurate and timely finance and accounting processes in a bank. None of these things are likely to be sources of sustained advantage, yet they all need to be done competently to ensure success. In the same way, good products and effective product management are critically important for all companies, even if not alpha assets for all companies.

Notes

- My central concept of alpha assets is essentially a reframing of the dominant intellectual paradigm in the academic field of competitive strategy, the resource-based view of the firm, first articulated comprehensively by Professor Jay Barney. Jay is an affable and enthusiastic man, now a professor at the University of Utah. We worked together on an interesting consulting project in healthcare, and have occasionally kicked around ideas on entrepreneurship, innovation, and teaching. The resource-based view (or RBV in the alphabet soup of obfuscating acronyms so often found in specialized fields) attempts to explain competitive advantage, and I think it does a pretty good job of doing so. But, it is far from clear. For instance, RBV argues that VRIN resources are the sources of competitive advantage. (Got it?) VRIN refers to valuable, rare, inimitable, and non-substitutable. (Got it now?) I made a good faith effort to use the VRIN framework in my book Innovation Tournaments (with Wharton colleague Christian Terwiesch), but it’s just too wonky for a non-academic audience. The resource-based view of the firm is both one of the most powerful ideas and one of the most poorly marketed ideas in social science. A makeover and rebranding is needed. As a first step, let’s just relabel VRIN assets as alpha assets, evoking some of the oldest tricks in branding, the use of alliteration, alphabetical primacy, the soft flowing sounds of a greek word, and the positive associations with the word alpha. Next, let’s simplify and make more intuitive the definition of VRIN. Alpha assets are (a) performance enhancing and (b) hard for others to obtain. This reframing now seems to work in the classroom, at least for me.

- While there are a lot of antecedents to RBV, this is the paper that explained the concept most clearly: Jay B. Barney, (1996) The Resource-Based Theory of the Firm. Organization Science 7(5):469-469.

- James Currier. The Network Effects Manual: 16 Different Network Effects – 2022 https://www.nfx.com/post/network-effects-manual Last accessed November 1, 2022.

- Peter Thiel and Blake Masters. Zero to One: Notes on Startups, or How to Build the Future. Crown Business. 2014.

Following is the note as a PDF document. You may use this note for non-commercial purposes with citation.

Here is the content in video format. I don’t think the graphics (which I did not create) are very good in these videos, so I suggest referring to my graphics in the note above. These videos are from my Wharton on-line course on Product Management and Strategy. Reach out if you need a referral in order to get a discount.