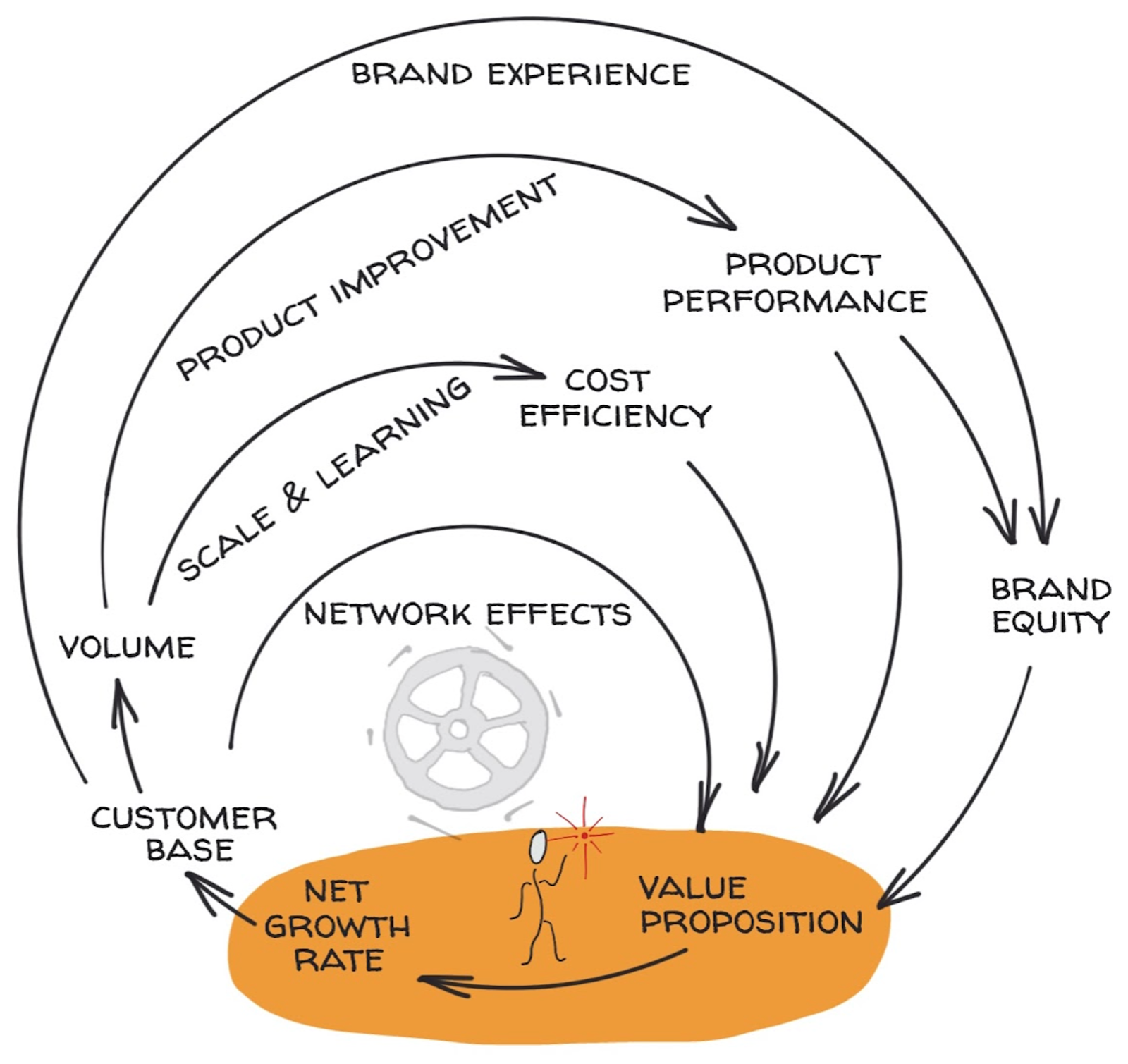

The five flywheels framework is admittedly mechanistic – even evoking the analogy of a machine. But the flywheels don’t operate entirely on their own. Managerial action is obviously important, and the flywheels exist within an organizational context with its own distinctive attributes.

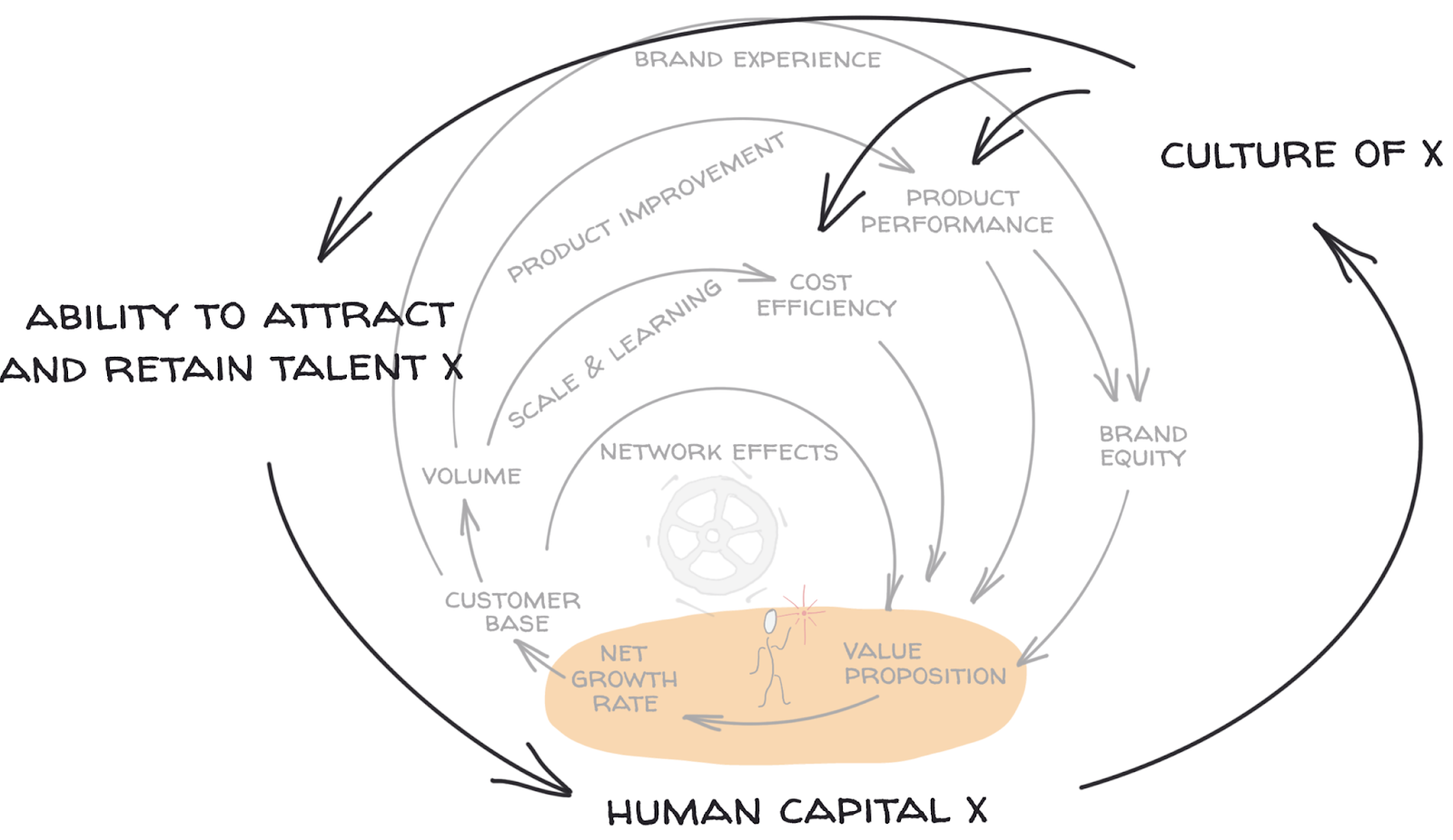

The JD Power organization ranks North American Hotels for guest satisfaction each year and The Ritz Carlton Hotel, a unit within the Marriott corporation, consistently tops the list for the luxury segment. Exceptional guest satisfaction is the brand promise that the Ritz Carlton makes to its customers, a significant element of the company’s brand equity. Some of the hotel’s ability to satisfy customers is the result of structured systems. For example, information technology allows any employee to make notes about guest preferences, creating an institutional memory that can be accessed in future guest interactions. However, much of its capability for delighting customers is the result of a culture developed and cultivated over decades within the Ritz Carlton organization. Ritz Carlton’s culture of guest satisfaction is itself a flywheel, distinct from but reinforcing of its brand equity. This culture is a flywheel in part because with cumulative time and experience, as with product performance or cost efficiency, the organization can ratchet incremental improvements. But even more significant, the culture is reinforced with positive feedback loops. As Ritz Carlton builds a stronger culture of customer service, the organization is better able to attract and retain employees with a propensity for delighting others, further strengthening its culture.

Although intangible, organizational attributes like a culture of customer service, are alpha assets because they both enhance performance and are hard for others to acquire – surprisingly hard. Consider that the Ritz Carlton’s parent company Marriott operates seven luxury hotel brands, including JW Marriott, St. Regis, and the W Hotels. Even other units within the same corporation have not been able to fully absorb the organizational capabilities of Ritz Carlton.

Deliberate managerial processes and their associated organizational culture can be thought of as lubrication and maintenance of the four flywheels: customer network, cost efficiency, product performance, and brand, and thus comprise a meta asset. A meta asset is an attribute that enhances a more fundamental and mechanistic alpha asset. These meta assets can themselves be flywheels.

Customer service is merely one of many possible organizational capabilities that could comprise a flywheel. I lump all of these organizational attributes under the label the fifth flywheel. I consider the fifth flywheel an organizational x factor, where x can assume many different performance enhancing attributes. The fifth flywheel can take many forms. Here are a few that I believe have proven to be particularly effective and worth describing in more detail. In each case, the organizational attribute associated with the fifth flywheel directly reinforces another important, albeit more mechanistic, flywheel powering competitive advantage.

Great Place to Work

Being an excellent place to work can be a fifth flywheel. NVIDIA Corporation is one of the very best places to work according to Glassdoor’s analysis of employee reviews and ratings. A typical review reads, “great culture around designing the highest performance products based on what can be done versus what is ‘good enough’.” NVIDIA relies on attracting and retaining extraordinary technical talent to design its video processing semiconductors. NVIDIA is not the largest semiconductor company in the world, but it can attract superior talent by developing a culture extremely attractive to the best engineers. By attracting that talent, it can create better products. Here’s the flywheel: the better the work experience, the easier it is to hire exceptional employees, improving the work experience even more. When attracting and retaining talent is critical to performance, being a great place to work can be a flywheel.

Company Values Aligned with Target Customer Identity

First, a counterexample. In 1986, Keith Richards founded Sierra Trading Post, selling discount outdoors gear. A core value espoused explicitly was a commitment to God, reinforced with Bible quotations on its packing slips. Richards’ commitment to Christianity almost certainly kick-started a flywheel, attracting a religious workforce, and further reinforcing the company’s commitment to God. However, that flywheel was not likely an alpha asset. In fact, the company’s target market segment was not exactly a God-fearing population, as reflected in animated threads about the company’s practices in online discussion forums among extreme outdoor enthusiasts. If anything, the company’s evangelism was a headwind against its other efforts to grow brand equity. When the company was acquired by TJX Corporation, the bible quotes were quickly scrubbed and today the company devotes substantial effort to communicating its commitment to religious diversity.

Now consider the outdoor gear company Cotopaxi. Co-founder Davis Smith built his company around doing good, with particular emphasis on enhancing the lives of individuals in extreme poverty in Latin America through improvements in health, education, and livelihood. Cotopaxi pursues this aim with fervor similar to that of Sierra Trading Post. Although Smith is himself religious, his company focuses on non-religious values that are directly aligned with its target market, and thus reinforce its brand equity.

The fifth flywheel is only an alpha asset when it directly or indirectly contributes to enhancing the value proposition of the company to its customers.

Continuous Improvement

The most valuable companies in the world are disproportionately technology companies with household names, including Apple, Microsoft, Amazon, Google, Tesla, and Tencent. But those companies cannot exist without another of the most valuable companies in the world, which most people have never heard of – TSMC, a semiconductor manufacturer with no chip designs or consumer presence of its own.

The very highest performance chips are now created by a partnership between a designer of the chip, say Apple, who does no production, and a semiconductor fabricator (a “fab”) who does no design. This is because manufacturing the chips themselves is so hard that it requires extreme focus and massive scale, two characteristics that can only be achieved by pooling the demand for chips from many device designers and devoting all organizational attention to one goal – relentlessly increasing the density of transistors on silicon wafers in order to continue to deliver on the promise of Moore’s Law.

Semiconductor manufacturing may be the hardest job to be done in the world. TSMC is currently the only company in the world that can make the microprocessors that power Apple’s latest iPhone or NVIDIA’s latest AI chip, and is currently on track to produce chips with features that are just 3 nM wide. How small is that? About 17 thousand times smaller than the width of a human hair. Transistors on chips can now be so small that Apple can put more than 100 billion of them in its latest microprocessor. Now imagine what is required to make 100 billion electronic devices 3 nM wide, which must each function perfectly in order for you to use Instagram on your iPhone.

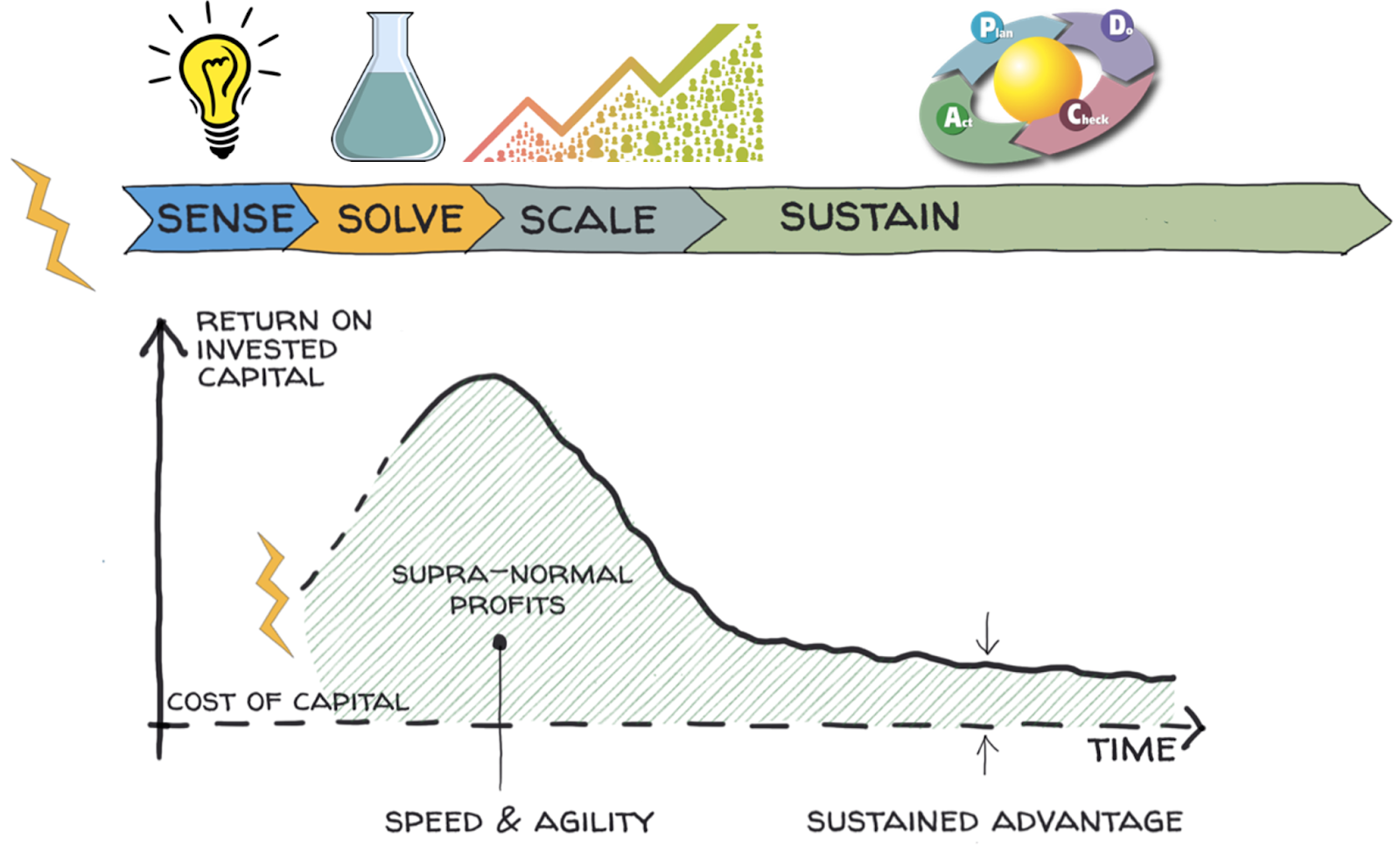

TSMC is built around a gigantic product performance flywheel. Its product, perhaps better described as a service or solution, is making chips. As solution quality improves, its value proposition improves, attracting the most demanding customers and increasing growth rate. Access to more demanding customers, greater scale, and increased experience further enhance solution quality. Now consider what organizational capability is required to lubricate this flywheel. An intense focus on one thing – process improvement. To give a sense of the size and scope of process improvements, consider that in 2021, TSMC filed almost 9000 patents and registered more than 20,000 trade secrets. The company has honed its process improvement and trade secret management system to a level that it now works to train others in its ecosystem and supply chain to make concomitant improvements themselves.

Adjacent Innovation

A few years ago I taught an MBA course on innovation in China which included a study tour of entrepreneurial companies in Beijing. One day we visited Xiaomi, a company that sells about as many smart phones each year as Apple. We spent the day talking with executives and touring facilities.The students also loaded up on colorful, zany, consumer products in the company store, with one commenting that Xiaomi was like Apple’s crazy cousin. Xiaomi fueled its meteoric rise to the Fortune Global 500 in just a decade by pursuing a strategy of prolific innovation around its core business of affordable high-performance smartphones running the company’s Android-based operating system MIUI. In addition to eight model lines of smartphones, the company’s product line includes tablets, laptops, home entertainment devices, electric scooters, small appliances, wearables, drones, and cloud services.

Although the company launches new products at a rapid clip, its innovation is extraordinarily bounded. There is no research on quantum computing at Xiaomi. Instead the company leverages a vital external ecosystem of users, developers, technology providers, and supply chain partners to reliably create a rapid-fire sequence of interesting and novel products, none of which represent a huge technological leap.

This innovation capability directly reinforces Xiaomi’s alpha assets of product performance and brand. This capability is also a flywheel with positive feedback – the more interesting Xiaomi’s products, the more desirable the company is as a place for innovative designers and engineers to work, and the more attractive it is as a partner for small inventive companies.

How did Xiaomi kick-start the innovation flywheel? The origin of Xiaomi was a big bang of talent. Founder, Lei Jun, key executives, and company communications staff all love to display a photo from the beginning of the company with a smiling Lei sitting on a conference table surrounded by seven seasoned leaders, several of them previous entrepreneurs, and combining experience from Microsoft, Google, and Qualcomm. Co-founder Liu De, educated at the elite ArtCenter College of Design in California, assumed the role of design visionary. It was a dream team of global innovators. They had learned an A game from the best global corporations and now focused their knowledge on one thing – efficient product innovation around a core operating system.

Lei Jun himself is an endlessly curious and open-minded leader. I recall visiting a Silicon Valley company with a unique production process for physical goods. I was surprised to learn that Lei had been there days earlier learning about the technology first hand. My sense is that Xiaomi does what Apple designers dream of doing when senior executives aren’t watching. The company acts like Apple might act if it had nothing to lose.

Dynamic Capabilities

The problem with flywheels is that they are, well, flywheels. Their job is to preserve momentum around a particular axis of rotation. What gives them the power to blast through barriers also makes them resistant to changes in direction. This is a good thing most of the time – companies that have found product-market fit benefit from a single-minded focus on ratcheting incremental improvements in product, cost efficiency, brand, and customer network. But, in highly dynamic industries, or in periods of significant industry disequilibrium, the companies that can adapt survive and thrive. This capability to reinvent capabilities is what scholar David Teece calls dynamic capabilities. He argues that this capability to change is itself a source of competitive advantage. Using my terminology, dynamic capabilities is a fifth flywheel.

Consider the software company Adobe. You know the company primarily as the source of portable document format or PDF, a widely licensed standard for encoding documents digitally. However, the bulk of Adobe’s revenue comes from the productivity tools used by creative professionals. These tools include Photoshop, Illustrator, Premier, and many others. Adobe has thrived since its founding 1982, but not without many periods of reinvention. Adobe’s first product was the postscript format used to represent documents for printers. Then, it created PDF. Then, it created a tool for manipulating images, Photoshop. As the world wide web developed, it acquired Macromedia corporation and provided the dominant tool for creating websites, Dreamweaver. Then, a tool for video, Premiere. As the world changed, Adobe changed with it. Likely the biggest disruptive threat for Adobe was the shift in the landscape from single-shot purchases of client software to cloud-based software-as-a-service monetized with subscriptions. In response, Adobe reinvented itself again, with the Adobe Creative Suite, a massive success, giving an all-you-can eat set of tools to creators for a reasonable monthly fee. When threatened by Figma, an easy-to-use collaborative tool for digital design, Adobe acquired Figma. This elephant can dance, and this agility is an alpha asset. Adobe’s ability to reinvent itself is clearly performance enhancing. But it is also vexingly hard for rivals to emulate. A culture of organizational innovation is the result of hundreds of actions taken over decades to reinforce reinvention as a core value, and to give the organization the specific tools and methods for changing itself.

Organizational Attributes are Sticky

It’s not hard to understand how organizational attributes like a culture of innovation can be performance enhancing. However, are organizational attributes really that hard for rivals to acquire? After all, there is no fancy technology or trade secret involved in a fifth flywheel. As most practicing managers know, organizational change is shockingly hard. Scholar Gabriel Szulanski did a fascinating study of the stickiness of organizational capabilities. What makes his work so interesting is that he studied the factors that explained the transfer of capabilities from one unit of a company to another unit in the same company. He found that even elements of know-how that substantially enhanced performance were resistant to transfer, even among sibling organizations. For example, telecommunications firm CENTEL had proven success with a process improvement methodology it called WPA, essentially a version of total quality management. When it attempted to deliberately transfer WPA to all units, the effort largely failed. Szulanski found that the key factors in predicting stickiness more generally are causal ambiguity, absorptive capacity, and arduous relationships among the transferring partners. Given how hard it is to adopt a practice from a sibling, imagine the challenge in adopting the organizational attributes of a rival.

Focus

Building organizational capabilities is hard, which is why they can be sources of advantage. The difficulty in spinning up the fifth flywheel is also the reason an organization can probably only possess one or two organizational attributes that are so exceptional they become alpha assets. Adobe would likely lose its edge if it attempted to focus on dynamic capabilities and on cost efficiency. There are three key reasons organizations must focus on just one or maybe two fifth flywheels.

Finite Resources

Social scientist Anders Ericsson did the research popularized by Malcolm Gladwell as the “10,000 hour rule,” which suggests that true expertise requires 10,000 hours of deliberate practice. Ericsson’s findings are much more subtle than Gladwell’s re-telling, but the essential truth is that being the best in the world at pretty much anything significant requires a huge investment of effort. Being the best in the world at more than one thing is exceedingly rare. This logic holds for organizations as well. Organizations have only so much managerial attention and free cash flow. Much better to be good enough on most dimensions and truly exceptional on the one dimension most reinforcing of performance. That one dimension might be customer intimacy, quality of the work experience, capability to innovate, obsession with process improvement, or alignment with values important to a target customer. Pick one.

Clear Communication

I bet you’ve heard the phrase “It’s the economy, stupid.” That’s what campaign strategist James Carville told campaign workers during Bill Clinton’s successful 1992 presidential campaign. Do you remember the second and third points in Clinton’s campaign? I didn’t think so. (They were “Change vs. more of the same” and “Don’t forget health care.”) The economy, change, healthcare – all important things. It’s a noisy world out there. You need every employee to understand what’s most important. Focus on one flywheel.

Decision Making Complexity

Imagine a bellhop at the Ritz Carlton trying to figure out the best course of action when a guest asks to store 12 pieces of luggage. Not a hard challenge when there is just one organizational value, customer satisfaction. However, imagine that the organization attempts to optimize both cost efficiency and customer satisfaction. What does the bellhop do? Consult a manual, calculate a trade-off, devise a fee for extra bags. Yikes. By then, neither objective is satisfied. To engender decisive action without bureaucracy, reduce the complexity of the objective. Of course some decisions require a lot of nuance. But, most don’t. Better to align an organization around the critical one or two objectives than to mire employees in complexity.

Levers on the Fifth Flywheel

Select a fifth flywheel carefully, preferring a focus on one that most enhances the value proposition to customers, as say the influence of organizational values on brand, or the influence of a culture of continuous improvement on cost efficiency. In selecting a fifth flywheel, also consider the beliefs and values of leaders. If you yourself are the company’s owner and CEO, what are your core values? If you are working to formulate strategy but report to more senior leaders, what are their core values? Yes, in theory, shareholders of a public company, via a board of directors, could select new leadership aligned with a desired fifth flywheel. But, most of us work in real situations that may deviate from theory, and may need to just assume organizational leaders are who they are.

Once a desired organizational attribute is identified, how can the associated flywheel be accelerated?

I remember a story my father told me when I was in high school. He worked as a consultant for Dupont and reported that someone at the lab that day had cut their finger with a box cutter. That minor injury launched the unit into action with an analysis of root causes and a plan for reducing the risk of recurrence. For Dupont, safety has been articulated as its primary core value for more than a century.

Davide Vassallo, when he led Dupont’s safety consulting unit articulated why safety is a fifth flywheel and alpha asset: “When you have good safety, that means you have control of your operations. And if you’re in control, of course you can drive business improvement as well.” Dupont went on to spin off a large and successful consulting firm DSS to deliver its safety solutions to companies around the world, an organization Vassallo now leads.

Dupont’s impressive success in creating its safety flywheel illustrates some effective methods useful for any organization.

Visible actions aligned with a North Star

The Chinese love short pithy sayings, usually four characters long, that they call “cheng yu.” My favorite is translated as “kill the chicken to warn the monkey.” Not exactly consistent with the Total Quality mantra “drive out fear,” but certainly reflective of the incontrovertible truth “actions speak louder than words.”

Employees are not stupid. The single most important lever for reinforcing a fifth flywheel is visible and costly actions that are aligned with a North Star. Absent those actions, no one believes. Conversely, when employees see an organization halt operations and investigate a cut finger from a box cutter, that action speaks much louder than the slogan “safety first” hung at the entrance of the laboratory.

When I was asked to serve as Vice Dean for Innovation at the Wharton School, then dean Tom Robertson allocated about ½ percent of Wharton’s revenues for unspecified exploration of opportunities to better pursue the School’s mission. Forming an innovation group, appointing a senior faculty member to lead it, and creating a multi-million dollar budget got the organization’s attention and was an honest signal that the School was serious about innovation.

Origin stories and myths

Dupont employees love to explain that Dupont’s culture of safety arose because the company started in 1802 with just one product, gunpowder. Frequent explosions were dangerous and disruptive. Founder E.I. Dupont committed to improvement, and built his own house in the blast zone of a potential explosion to reinforce his commitment to employee safety.

Although not as dramatic an origin story, consider how Amazon employees recount their founder Jeff Bezos making the company’s desks from doors and framing timber to minimize costs. That story is a founding myth that reinforces the company core value of cost efficiency.

Codification in processes and systems

Dupont includes an evaluation of safety practices in its performance reviews. In the 1960s, Dupont started selling its safety services to other companies, and developed structured processes for risk assessment and safety improvements.

When Adobe committed to improving its culture of innovation it created the Red Box. <more…>

Processes and systems aligned with a fifth flywheel reduce friction and increase momentum, and no flywheel can spin when faced with the friction of processes and systems at cross purposes with a desirable attribute of organizational performance.

Communications and manifestos

Dupont’s corporate communications reinforce its core values. Safety is listed first.

You’ve probably heard of Netflix Founder Jeff Hastings’ 2001 Powerpoint presentation about Netflix values. It’s a highly public manifesto of what matters at Netflix, or at least what mattered in the early 2000s. A fifth flywheel is clearly articulated on slide 21, “A great workplace is stunning colleagues.” And then on slide 23, “Adequate performance gets a generous severance package.” Whoa. Got it. When a company releases a detailed document viewed tens of millions of times and containing extraordinarily specific and distinctive desired elements of culture, the company torques the flywheel.

Investment in education, training, and deliberate practice

Dupont makes significant and deliberate investments in education and training. For example, in order to influence employees beliefs and cognitive models about safety, it created a system called DnA (Dupont Integrated Approach) that was implemented with a 2-day training program for the plant managers, a 2-day program for mid-level supervisors, focused coaching sessions for all leaders, managers, and supervisors; a 4-hour training program for all plant-floor workers; and then periodic on-going skills workshops for supervisors.

For elements of culture to stick, they require continual reinforcement and visible investment in education and training.

Notes

Senge PM (1990) The Fifth Discipline: The Art and Practice of the Learning Organization (Currency, New York).

Szulanski G (2003) Sticky Knowledge: Barriers to Knowing in the Firm (SAGE Publications, London).

https://www.mi.com/global/about/founder/

(Accessed November 21, 2022)

Apple M1 chip

https://en.wikipedia.org/wiki/Apple_M1

(accessed November 22, 2022)

DuPont Origin story

https://www.dupont.com/news/safety-at-our-core.html

Accessed November 16, 2022

Dupont Values

https://www.dupont.com/about/our-values.html

Accessed November 16, 2022

Dupont training (DnA) program

Accessed November 16, 2022

Bloom et al 2020 AEA

Adobe Red Box

Dupont spins out DSS as its own business

https://cen.acs.org/safety/DuPonts-safety-segment-solo/97/i12

Netflix Reed Hastings 2001

Accessed November 16, 2022

Anders Ericsson and Robert Pool, Peak: Secrets from the New Science of Expertise.

Michael Treacy. Discipline of Market Leaders.

Wikipedia “It’s the Economy Stupid” (accessed November 15, 2022)

https://en.wikipedia.org/wiki/It%27s_the_economy,_stupid

https://www.glassdoor.com/Reviews/NVIDIA-great-culture-Reviews-EI_IE7633.0,6_KH7,20.htm

Accessed November 14, 2022

Keith Richards (Sierra Trading Post founding story)

Wayback machine April 4, 2003 version of http://www.sierratradingpost.com/StaticText/CompanyHistory.asp?wc=true

https://www.tetongravity.com/forums/showthread.php/54383-Does-the-whole-jesus-and-STP

(animated debate about christianity and outdoor gear)

https://www.tjx.com/responsibility/workplace/inclusion-and-diversity

TJX corp diversity and inclusion – religious diversity

Founding story (http://www.sierratradingpost.com/lp2/founding_story.html):

“Harder than the planning was deciding how to commit a business to God. To do this, we ensure that this business reflects God’s principles in the way we treat employees, vendors and customers. Each catalog includes three “We believe” statements. In addition, we print a quotation from the Bible on our order blank. These statements serve to hold me accountable.”

{kind=link}

{kind=link}